Chairman and group ceo’s

joint statement

The growth in the O&G Division was mainly due to the

successful execution of major projects. The projects

include the Petronas EVA-NMB gas delivery system

contract worth RM232.1 million, which was completed

in the third quarter of financial year 2014 and the on-

going execution of the Polarled Development Project,

for Statoil, worth USD$198.0 million.

On the strategic investment front, Wasco acquired a

49% stake in Alam-PE Holdings (L) Inc. (“Alam-PE”)

for RM106.0 million. Alam-PE is a company engaged

in ship-owning and chartering of offshore support

vessels and ship management services. With the

successful acquisition, Wasco had positioned itself

to gain a longer-term, sustainable and stable income

stream. This together with the existing investment in

Petra Energy Berhad is expected to generate recurring

earnings stream in the longer term to supplement the

current project based earnings stream.

A licensing collaboration was signed between

PETRONAS and Wasco in December 2014, whereby,

Wasco was given the exclusive rights to market, sell,

supply and apply REMCOAT™, a PETRONAS proprietary

product for pipeline coating.

Whilst the O&G Division achieved its best performance,

2014 ended on a sombre note with oil prices falling

substantially in the final quarter of the year. The

falling oil prices have temporarily clouded the O&G

landscape. However, the current oil crisis is not

unlike the ones we have seen in the past, where we

had managed to weather the economic uncertainties

brought about by weakening oil prices. We have

already begun to proactively manage the imminent

slowdown – our continued focus towards looking into

strategic investments and partnerships is just one of

the many steps we have undertaken to avoid cyclical

fluctuations. Against this backdrop, Wasco remains

steadfast in facing the challenges ahead.

RENEWABLE ENERGY DIVISION

The RE Division delivered a commendable performance

for the year under review, recording revenue of

RM342.5 million and segment profit before taxation

of RM62.1 million. The growth in RE’s business was

primarily due to increase in sales of steam turbines,

boilers and kernel crushing plants for palm oil and

agro-based industry.

In 2014, the Division made various key notable

achievements. The Division’s waterfront expansion

project in Telok Panglima Garang, Selangor is already

in its 2

nd

phase of development. It is targeted to be

completed by end of 2015 and will result in engineering

fabrication facilities with a combined production

capacity exceeding 20,000 metric tons. With the

development of the new waterfront fabrication facility,

it will also be capable of fabricating bigger engineering

structures and modules. The Division achieved a

milestone following the successful sales of the 1,000

th

unit of Shinko steam turbine by PMT Industries Sdn

Bhd (“PMT”). Building on its long experience in the

palm oil industry, PMT undertook a turnkey contract

to build and commission a 15MT palm oil mill in

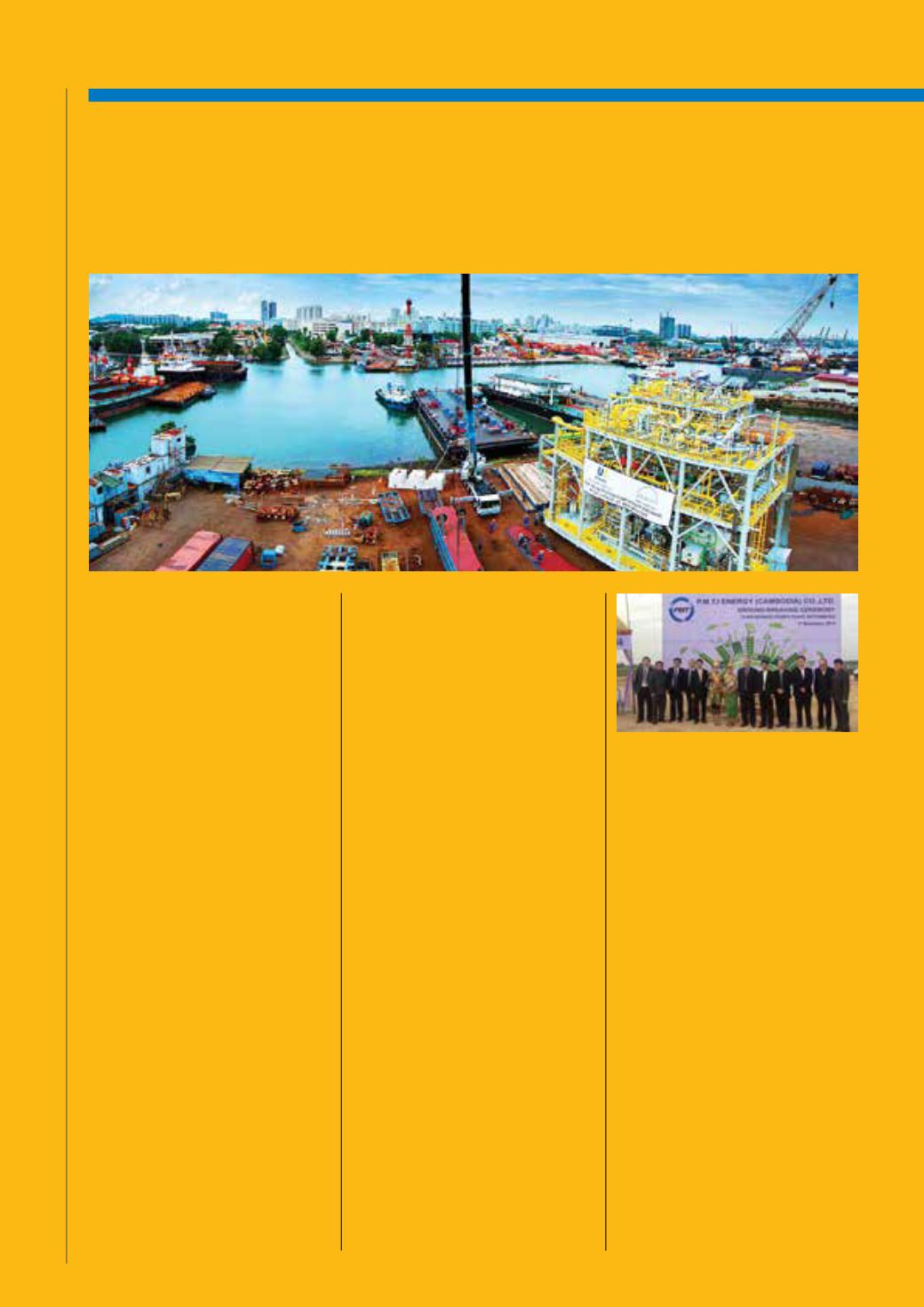

Honduras. The Division also cemented its footing in the

biomass power generation sphere in Cambodia with its

first rice husk biomass power plant under the “Build-

Own and Operate” model. Plans to supply power to

Cambodia’s national grid are on target and expected to

be commissioned in 2016.

Looking at year 2015, the O&G and Petrochemical

sectors are expected to be the main contributors

to the Division’s revenue, capitalising on Petronas

RAPID project at Pengerang. The strategic

partnership with Shinko Ind. Ltd. and successful

launch of the steam turbine manufacturing line at

our Shah Alam facility will enable the RE Division to

be more competitive by enhancing capabilities to

play a key role in manufacturing and distributing

Shinko steam turbines in the Asean region and

worldwide. In order to fulfil and sustain WSC’s

RE Division’s strong track record in servicing industries

across the world, we made inroads into new overseas

market, such as the Latin America, East Asia and Africa.

INDUSTRIAL TRADING & SERVICES DIVISION

For the year under review, ITS Division recorded a

revenue of RM595.2 million and lower segment profit

before taxation of RM6.6 million. Financial year 2014

was a challenging year for the ITS Division particularly

for PPI Industries Sdn Bhd (“PPI”) where many targeted

infrastructure and water pipes projects were delayed or

shelved, despite an improvement from the previous

year due to better sales margin. Meanwhile, Syn Tai

Hung Trading Sdn Bhd (“STH”) saw a decline in revenue

primarily due to a planned reduction in steel bar sales.

This was part of its strategies to shift the company’s

product mix towards higher margin strategic products.

The operating environment for the ITS Division

is expected to be challenging in year 2015. The

Management is cautious on the various current

issues that could affect its trading business such as

the impact of the GST implemented in April 2015 and

the slowdown in property development nationwide.

Measures introduced by Bank Negara to tighten

6

Wah Seong Corporation Berhad • Annual Report 2014